Determining the price is an essential aspect of a company handover and one of the most difficult steps in this process. It is always fundamental to distinguish between the value and the price of a company. An article by Bruno Leibundgut on some of the different approaches.

Pricing is probably one of the most important tasks in planning corporate succession. Even if the focus is on securing the company’s existence rather than maximising the price, the actual value of the company remains a core issue. It should, of course, be determined as realistically and objectively as possible before the actual price will also be influenced by subjective factors.

A company’s value may fluctuate greatly depending on the internal or external parameters applied or on the individual views of the parties involved. Depending on the occasion for the valuation (sale of the company, merger, etc.) or the starting situation (size and age of the company, its capital and asset structure, etc.), different calculation approaches are used.

The following approaches can be used to determine a company’s value according to objective criteria:

- Asset-based approaches

- Income-based approaches

- Practical approach (combining asset-based and income-based approaches)

- Market-based approaches / using multiples

However, this list is not exhaustive and some of the approaches listed have different variants. Explaining them in detail would go beyond the scope of this blog post. Therefore, we will focus on some useful advice that will facilitate a company valuation regardless of the approach used.

First, the balance sheet and the income statement should be adjusted to show the balance sheet and operating result in an economically objective manner. Non-operating assets are to be distributed or outsourced. This is especially important as the intention is to transfer operations only. The figures thus obtained usually differ from the company’s official annual accounts, as these are often influenced by tax considerations and include value adjustments or provisions. Moreover, in the case of an SME, the owners’ wages are another issue that must be taken into account when adjusting the income statement. To avoid surprises on any side, the compilation of all these statements must be made a top priority.

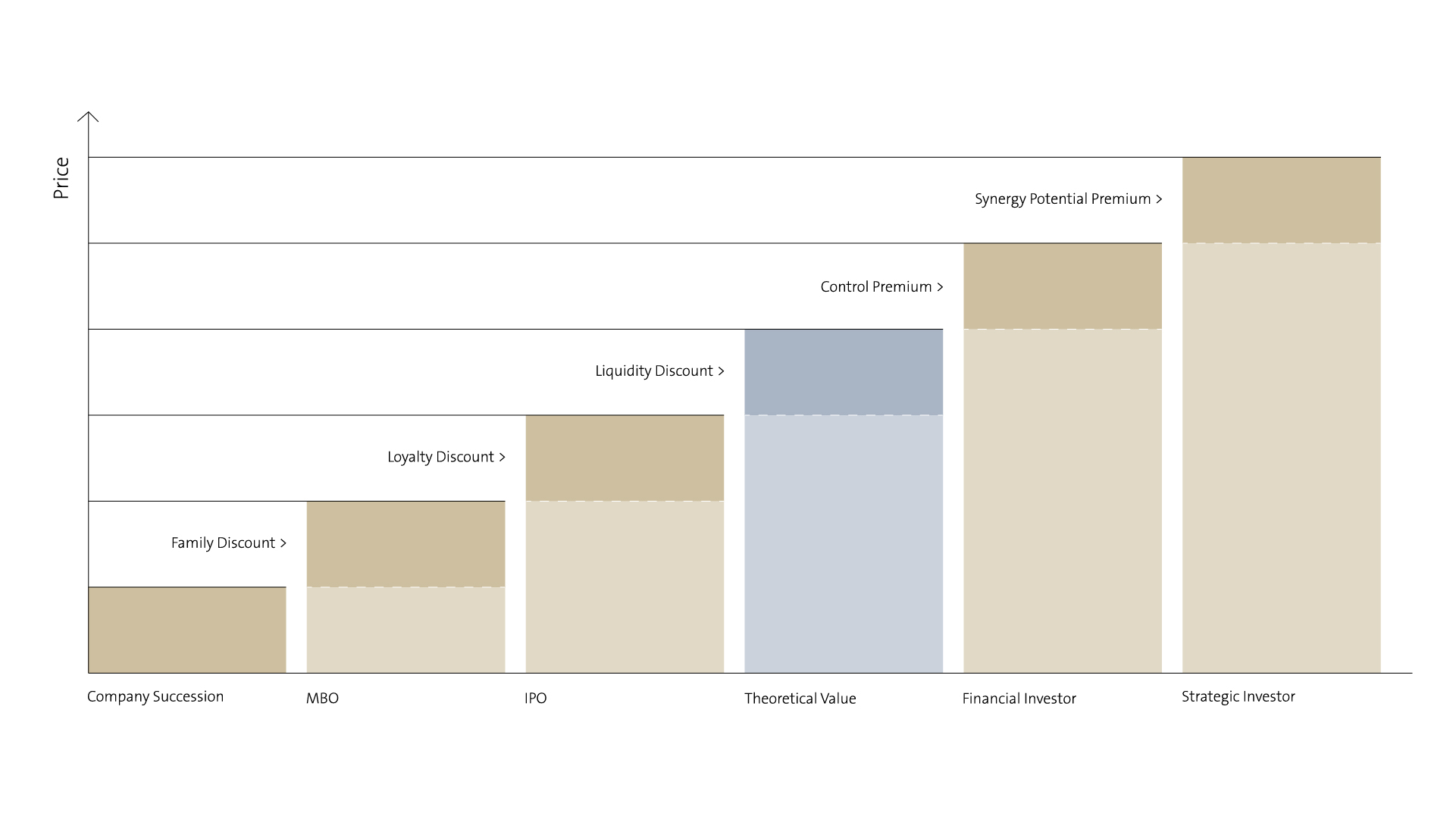

Once a preliminary company value has been determined, various factors will influence the final price. Does the company remain within the family, is it passed on to someone in management or to a competitor or investor? It makes sense to compare several of the above-mentioned valuation approaches during the pricing process. In addition, it is helpful to examine the company out of the buyer’s perspective and to look for a clearly identifiable company profile. This makes it easier to justify the determined price. If the transaction promises great synergy potential or if you are selling to a competing company, the price may be higher than the objective company value. However, if the objective is to secure the company’s continued existence, the price may be lowered, and a discount accepted.

At Experfina, we have in-depth expertise on this topic and will be happy to guide you through the various steps of your succession process or the respective preparations and financing issues.

{kind=link}

{kind=link}